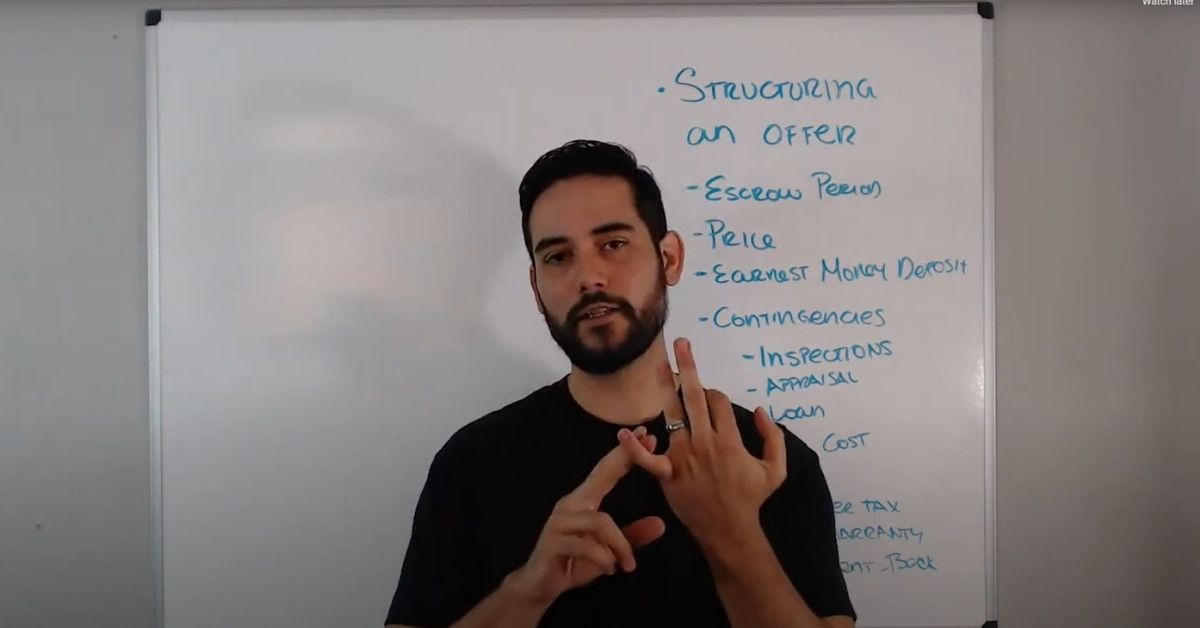

This video, we’re going to go over how to structure an offer. And we’re going to be covering some of these items in much greater detail in the subsequent video, but this is kind of the 30,000-foot overview of things to consider.

So really starting with the escrow period, this is something that I, as your agent or somebody on our team will work with your lender to determine what is realistically the window of time, the shortest window of time that you need in order to fully close this loan out or this purchase out.

And so we go, as I mentioned, in a previous video, we’ve seen anything as short as 15 days with a financed offer to 30 days. We rarely go beyond 30 days, but on average, we’re seeing about a 21 day escrow period, meaning that from when they accept the offer until when you get keys, it’s about a 21 day period.

And so from there, we’ll coordinate with your lender regarding what that timeframe needs to be. And depending on how competitive we have to be if there are other offers that are slightly more competitive, a shorter escrow might be helpful.

We’ll take into consideration as well that this is an estimated timeframe, so inevitably there might be things that come up that can push things a little bit further out. It’s my job or whatever agent you’re working with on our team to be in constant communication with the listing agent so that we’re getting ahead of any potential delays.

I rarely have found it an issue but most people are very understanding of any kind of reasonable delays and so that’s going to be something that we’re going to be actively working on your behalf. So know that even if we say 21 days and it comes out to be 25 it’s not a problem.

The next item on the contract’s going to be the price! As mentioned in my previous video, to establish this we’re going to provide a comparative market analysis. This is where we’re going to take a look at what comparable homes sold for in the area around your home of interest to establish a base or a range of what we feel confident the home is going to appraise for. This will set a ceiling for your loan (we’ll discuss this in more detail in a separate video).

So the price will be the next piece from there. It’s fairly standard in Sacramento that the earnest money deposit or EMD amounts to 1% of the offer price.

So if you’re offering $450,000, your earnest money deposit is going to be $4,500. If you’re offering $350,000, it’s going to be $3,500. The earnest money deposit, essentially is your skin in the game, your commitment to buying this home. And your earnest money deposit needs to be provided to the title company within three days of an accepted offer.

Once we get an accepted offer, the listing agent will send a whole packet over to the title company and the title company will reach out to us. We’ll send them your contact information and they’ll reach out directly to you to provide you with the wiring instructions for the deposit.

Note that wiring the deposit is optional but it is the most time-efficient option. I encourage you to talk to your bank to determine what that process looks like and what the timelines are for it. Sometimes banks can do the same day and sometimes it’s 1 – 3 days, and so you kind of want to figure that out ahead of time.

You can also write a money order or cashier’s check that you physically drop off to the title company. I wouldn’t encourage mailing it unless you’re out of town or just absolutely can’t do it via wire.

On rare occasions, you can also provide the deposit via a personal check, but that’s an absolute last option. In some cases, you might have sellers that will want a higher earnest money deposit when a personal check is used. Just note this changes nothing for you because, at the end of the day, this deposit gets applied towards your closing costs or your down payment for the home purchase.

So for example, I just helped a client get into contract on a home where they offered $459,000, and so their earnest money deposit was $4,559 (rounded up it would be $4,600). But the listing agent was not from this area and requested an earnest money deposit of $7,000 instead. Fortunately, that was not an issue for my clients and so we conceded on that because, at the end of the day, it’s going to be applied towards their down payment and closing costs.

Next, we have contingencies: inspections, appraisal and loan. This is an area that we’re going to go into much greater detail about in another video because there’s a lot to cover in this area. For now, know that the contingencies help by telling us how long of a period we will have to review the documents for all of our inspections. Common inspections included: Home, Pest, Roof, HVAC, and Sewer. Typically the standard contract timeline is 17 days, and usually, I am able to secure inspections and reports for about 90 to 95% of my contracts within 10 days.

Sometimes there’s a little bit of delay, but again, it’s the job of myself and my team to proactively communicate with the listing agents to coordinate any potential delays and get ahead of them.

With the appraisal contingency, we don’t have as much control over when that gets done. Once we receive an accepted offer, we’ll submit a request to what’s called an appraisal management company. They’ll put it out to the field and an appraisal appraiser will accept the job. Sometimes that happens within a few days of that request being sent out, sometimes it takes a week. Then it can take another five to seven days before we actually get that report. We have a little bit less control over what that timeline looks like, but nevertheless, 14 days seems to be a fairly reasonable timeframe for which to expect that to be completed.

And finally, the loan contingency. You might ask if I have a pre-approval with a loan company why do I still have to go through another approval process? Once you get into contract, there are a lot of pieces to the puzzle that are related to specific property that has to be taken into consideration by the loan underwriter to approve your final loan. And so they will compile that information and review everything until they can confidently fund your loan.

And that’s where you go through that secondary approval process for your loan… continue to the next video for part two.

Leave a Reply