…[continued from Part One] and so once the underwriter gives us that thumbs up, then we can release that loan contingency. Contractually the general contract timeline is 21 days.

Typically we’re able to get that done within 15 to 17 days based on getting all the documentation from you as a buyer and from the listing agent for the property, to be able to get that to the underwriter and for them to be able to clear whatever items they need to clear.

At that point, those are the three contingencies. Each one of those presents an off-ramp. So if we come across anything in the documentation or the physical inspections, that’s a big concern and we bring it to the attention of the seller and we attempt a negotiation and we just can’t find a point of agreement, that’s an off-ramp and we get your full earnest money deposit back at that point.

If there’s no issues that we need to negotiate or we’ve negotiated and everybody’s on the same page, we’ll release our inspection contingency. We can no longer get off using that off-ramp.

Now there’s the appraisal, which we’ll go over in more detail, but ultimately the home has to appraise at the offer price or if it appraises below. Then we have to try to figure out kind of what, how are we going to handle that with the seller?

And I’ll go over some strategies in another video, but ideally let’s just hypothetically say that it’s either coming at value or if it came in below but we’ve reached a point of agreement and we’re comfortable moving forward, don’t worry about it appraising above.That’s actually great. That just means that you have instant equity in the home, so you never have to move your price up just because it appraises at more than what you offered.

So that’s the appraisal. And so once we reach a point of agreement on that, we release the appraisal contingency and we’re no longer able to get off that off-ramp anymore. If we don’t come to a point of agreement, then that’s an opportunity for us to just say, you know what, I’m sorry, but we need to back out of this and we get your earnest money deposit back, the final contingency is the loan.

So if there’s some kind of crazy unexpected event that results in you losing your job or some kind of an impact on your ability to qualify for the loan, of course, they’re not going to give that final approval. At that point, we just say-

“We’re sorry, this unexpected thing came up and we are no longer eligible for a loan. And so we have to pull out of this process. We had every intent of closing this, but we are no longer able to do so.”

That’s the final kind of off-ramp that if we do have for ourselves. We communicate that, and we get your earnest money deposit back and move on.Once we release that though, the loan, once we release all three contingencies, there are no more off-ramps at that point, we’re moving forward to a close.

And so again, that’s why it’s important for us to talk through these details and why we’re going to go into much greater detail in another video for these.

And then finally the closing cost. So here you have within the contract, the terms that will dictate who takes on what costs associated with the closing of the contract.

So in the Sacramento area, it’s pretty common. It’s standard, to split the title Fee 50-50. And so that’s between the seller and the buyer. If you want to make a very competitive offer, you can take it on but it’s standard for it to be split 50-50 on the transfer tax.

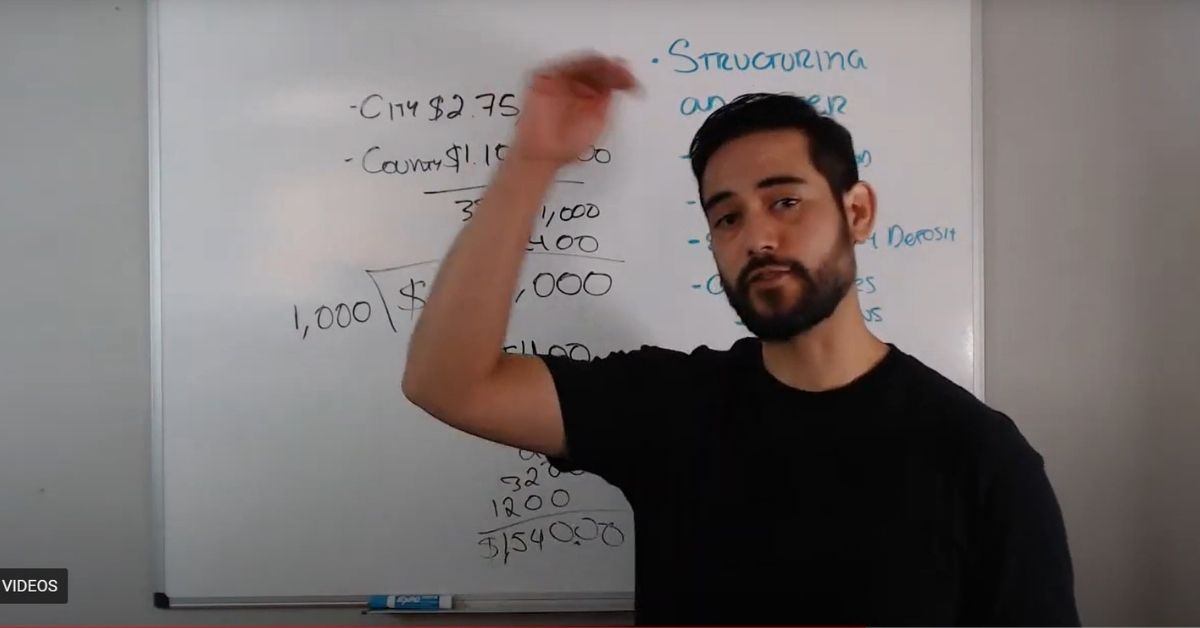

So when it comes to the transfer tax, there’s two components that go into that. The transfer tax is a tax charged- if you’re subject to the city or within the boundaries of the city, you have a city transfer tax is $2.75 cents for every thousand dollars. The county is a $1,10 for every thousand dollars. So the total is $3.85 cents if you’re subject to both the city and the county, and depending on where you’re buying, if it’s west SAC, it’s a little bit different, if it’s Rancho Cordova area, it’s a little bit different. And so, you know, we, we’ll kind of base it on where you’re buying.

And so $3.85 cents for every thousand dollars. What this means is that for the purchase price, let’s just say hypothetically, it’s $450,000 or for ease of math, we’re going to call it $400,000 is what we offer on the house. You divide that by a $1,000, you get $400. You then multiply that $400 by the $3.85. Making the total transfer costs for the home at $400,000 is $1,540.

If you offered to split, you know, that just kinda shows a collaborative spirit in your offer, you would split that. So your portion would be $770. If we’re having to compete against a lot of other offers, that’s an opportunity for you to be more proactive and say, we’ll take that on. If that’s something that you’re able to do, because that just gets added to your closing costs and your cash to close will grow based on that number. So that’s the transfer tax.

The home warranty is something that can be asked for. It’s fairly standard to ask for the seller to give you a credit for that. It ranges anywhere from $385 to 545 depending on the company. And it’s kind of up to you. If it’s something that gives you additional peace of mind. It’s different from home insurance, home insurance covers a structure, home warranty typically covers mechanical items, but the mechanical items have to be in proper working order in order to fall under warranty, if aware of any defects for example with the HVAC, and you buy the home warranty in the hopes that when it dies, you can use it, more than likely you can’t.

And so it’s a bit of a mixed bag with regard to the need for a home warranty, but just know it’s something that if we’re being competitive, I would advise you waive it. You can still buy it, but at the end of the day, we want our numbers to beat up any other offers numbers. And so sometimes waiving that $585 will make a difference. Finally, and this I’ll go into detail in another video.

In some cases, a seller will need some time because they are in the process of purchasing a home themselves and are still in the process of looking or in the process of closing. They may need a period after the close of your escrow to remain in the house. And so I’ll go over this in much greater detail, but that’s sometimes what wins out against other offers that don’t have that flexibility to offer something like that in there.

But these are the key items that would be taken into consideration when we’re putting together an offer. And of course, every single home that we write an offer for is going to be required unique combination of these.

And so we’ll be able to talk about it as we come across homes that you really want to make your own and make sure that we structure the strongest possible offer for you based on the home and based on any competition that we’re aware of. Hopefully this was helpful. If you have any questions again, I’m going to be covering some of these in much greater detail in subsequent videos, but don’t hesitate to reach out and I’ll see you on the next one.

Leave a Reply